")

Sending a parcel across Australia should be a moment of excitement, not a source of stress. Courier insurance is that all-important safety net, the one thing that stands between your business and a potential financial hit if a shipment gets lost, damaged, or stolen on its journey. It’s what transforms a would-be disaster into a manageable hiccup, keeping your business strong and your customers happy.

Your Guide to Secure Shipping

Picture this: a small online jewellery store in Melbourne sends a stunning, custom-made necklace worth $1,500 to a client in Perth. Somewhere across the vast Nullarbor, the delivery van has an accident, and the package vanishes. Without the right insurance, that business owner is stuck with a terrible choice—either wear the full cost of replacing the necklace or risk losing a loyal customer forever. It’s a stark reminder that for any Australian business sending goods, risk is just part of the game.

This guide is here to take the confusion out of insurance and turn it into one of your biggest assets. We're going to break it all down, step by step, so you can protect every shipment with total confidence.

By the end, you'll have the know-how to:

- Understand Different Policy Types: Get clear on the crucial differences between the basic liability a courier offers and proper, comprehensive extra cover.

- Navigate the Claims Process: We’ll give you a straightforward roadmap for getting your claim sorted without the usual headaches.

- Minimise Your Risks Proactively: Learn the best practices for packaging and paperwork that can stop problems before they even start.

- Make Cost-Effective Decisions: Understand how premiums, excesses, and coverage limits really affect your budget.

Turning Risk into a Competitive Advantage

Think of this guide as your playbook for building a rock-solid shipping strategy. Good insurance isn't just a defensive move; it's a launchpad for growth. It gives you the confidence to ship high-value items, reach new customers right across the country, and build a reputation for being utterly reliable. When you get a handle on courier insurance, you’re free to focus on what you do best: delighting your customers and growing your business.

For courier businesses using smaller electric vehicles for those last-mile deliveries, a specific guide to Low Speed Vehicle insurance provides vital details on getting the right coverage for your fleet. This kind of specialised knowledge ensures every angle of your operation is properly protected. As you refine your shipping strategy, understanding these nuances is crucial. Learn more about how to choose the right courier for your needs in our detailed article.

Understanding the Foundations of Freight Protection

When you send a parcel across Australia, you’re placing your trust in a complex network of vehicles, sorting depots, and dedicated people. To protect your goods on their journey, you need to get your head around the two main layers of protection available: insurance for couriers. Don't think of these as complex legal traps; see them as two different levels of a safety net, each built for a specific job.

The first layer is what's known as included carrier liability. This is the standard, base-level cover that a courier company like Aeros Couriers provides as part of its everyday service. It’s a bit like the standard manufacturer's warranty that comes with a new appliance—it covers certain, limited situations up to a fixed amount. This is your first line of defence, but it’s not designed to cover the full retail price of every single item you ship.

Then you have the second, more comprehensive layer: optional extra cover. This is a separate, dedicated insurance policy you can choose to purchase for total peace of mind. Using our appliance analogy again, this is like buying the extended warranty that covers accidental damage. It offers far broader protection, often for the full value of your goods, and shields you from a much wider range of potential mishaps. It’s the only way to go for high-value or one-of-a-kind items.

Understanding this difference is more crucial than ever. The Australian freight insurance market was valued at an incredible USD 1,593.94 million in 2024 and is expected to soar to USD 2,314.23 million by 2033. This isn't just a number; it shows how vital solid protection has become for businesses trying to thrive in today's supply chains. You can dig into the specifics in this in-depth analysis of the Australian cargo insurance market.

To help clarify the differences, let's break it down side-by-side.

Included Insurance vs Optional Extra Cover at a Glance

This table offers a clear comparison between what's typically included as standard and what you get when you opt for additional cover.

| Feature | Included Carrier Insurance | Optional Extra Cover Insurance |

|---|---|---|

| Coverage Basis | Based on weight (e.g., per kilo) or a set item limit. | Based on the declared value of your goods. |

| Typical Limit | Low, capped amounts (e.g., up to $100-$1,500). | Higher limits, often up to the full declared value. |

| What's Covered | Generally covers loss or damage due to carrier negligence only. | Broader coverage, including accidents, theft, and other perils. |

| Exclusions | Many exclusions, such as insufficient packaging or prohibited items. | Fewer exclusions, though conditions still apply (e.g., acts of God). |

| Cost | Included in the standard freight charge. | Additional premium based on the value of the goods. |

| Best For | Low-value, easily replaceable items. | High-value, fragile, or mission-critical shipments. |

Ultimately, choosing the right cover comes down to a simple risk assessment: what's the real-world cost to your business if this specific parcel goes missing or arrives broken?

Declared Value: The Key to Your Payout

There’s one concept that links both types of cover, and it’s absolutely critical: declared value. When you book a courier, you state how much the item is worth. That figure becomes the absolute ceiling for any claim you might make.

Getting this right is non-negotiable. If you try to save a few dollars by under-declaring the value of your goods, you’re also slashing the maximum payout you could receive. It’s a gamble that can leave you severely out of pocket. Honesty and accuracy are your best friends here.

The Chain of Responsibility: A Shared Duty

Here in Australia, shipping isn't just about sticking a label on a box. It’s a regulated industry governed by the Chain of Responsibility (CoR) laws. This framework makes it crystal clear that everyone in the supply chain—from the business sending the goods to the driver behind the wheel—shares a legal responsibility for safety.

Key Takeaway: The Chain of Responsibility means you, the sender, are legally on the hook for making sure your goods are packed, labelled, and declared correctly for safe transport. Having the right insurance is a massive part of fulfilling that duty.

This shared accountability is exactly why understanding your insurance options is so empowering. When you choose the right level of cover, you're not just protecting your bottom line. You're upholding your legal obligations and helping create a safer shipping environment for everyone. It shows a level of professionalism that builds trust with your courier and, most importantly, with your customers. To get your parcels moving the right way, learn more about our domestic freight express services.

This simple map shows just how powerful the right insurance can be for your business, giving you the foundation to build resilience and grow with confidence.

As you can see, good insurance isn't just a cost—it's a strategic asset that underpins your business continuity, gives you genuine peace of mind, and frees you up to focus on what you do best.

What Your Courier Insurance Actually Covers

Knowing what your policy protects is the difference between genuine peace of mind and a false sense of security. Think of your courier insurance as a shield—it’s strong, but it has defined edges. Understanding where those edges are is what empowers you to ship with real confidence, so there are no nasty surprises if you ever need to rely on that protection.

At its heart, courier insurance is there to cover the financial hit if your goods are lost or damaged while in the courier's hands. This is your safety net against the bumps and scrapes of the transport world.

It generally kicks in for things like:

- Damage from Carrier Mishandling: This is for items broken because they were dropped, sorted incorrectly, or otherwise mishandled by the courier's team.

- Transit Accidents: If the delivery van gets into a prang and your goods are wrecked, your policy is there to step in.

- Theft: This covers your package being stolen from a courier vehicle or a secure depot while on its way to your customer.

Unpacking the Common Exclusions

Just as crucial as knowing what’s covered is knowing what isn’t. Insurance policies aren't a blank cheque; they have specific exclusions that stop a claim in its tracks. These aren't sneaky traps—they're standard conditions designed to keep things fair and encourage everyone to ship responsibly.

Being aware of these exclusions is your best line of defence against a denied claim. More often than not, they relate to situations where the sender’s own actions (or inaction) played a part in the loss.

Crucial Insight: Think of an insurance policy as a partnership. The insurer agrees to cover the risks of the journey, but you, the sender, agree to prepare the goods to survive it. A denied claim often happens when one side of that bargain isn't met.

Inadequate Packaging: The Number One Hurdle

This is, hands down, the most common reason claims get knocked back. It’s your job to pack items well enough to handle the normal rigours of modern logistics. That means surviving automated sorting machines, road vibrations, and being handled alongside countless other parcels.

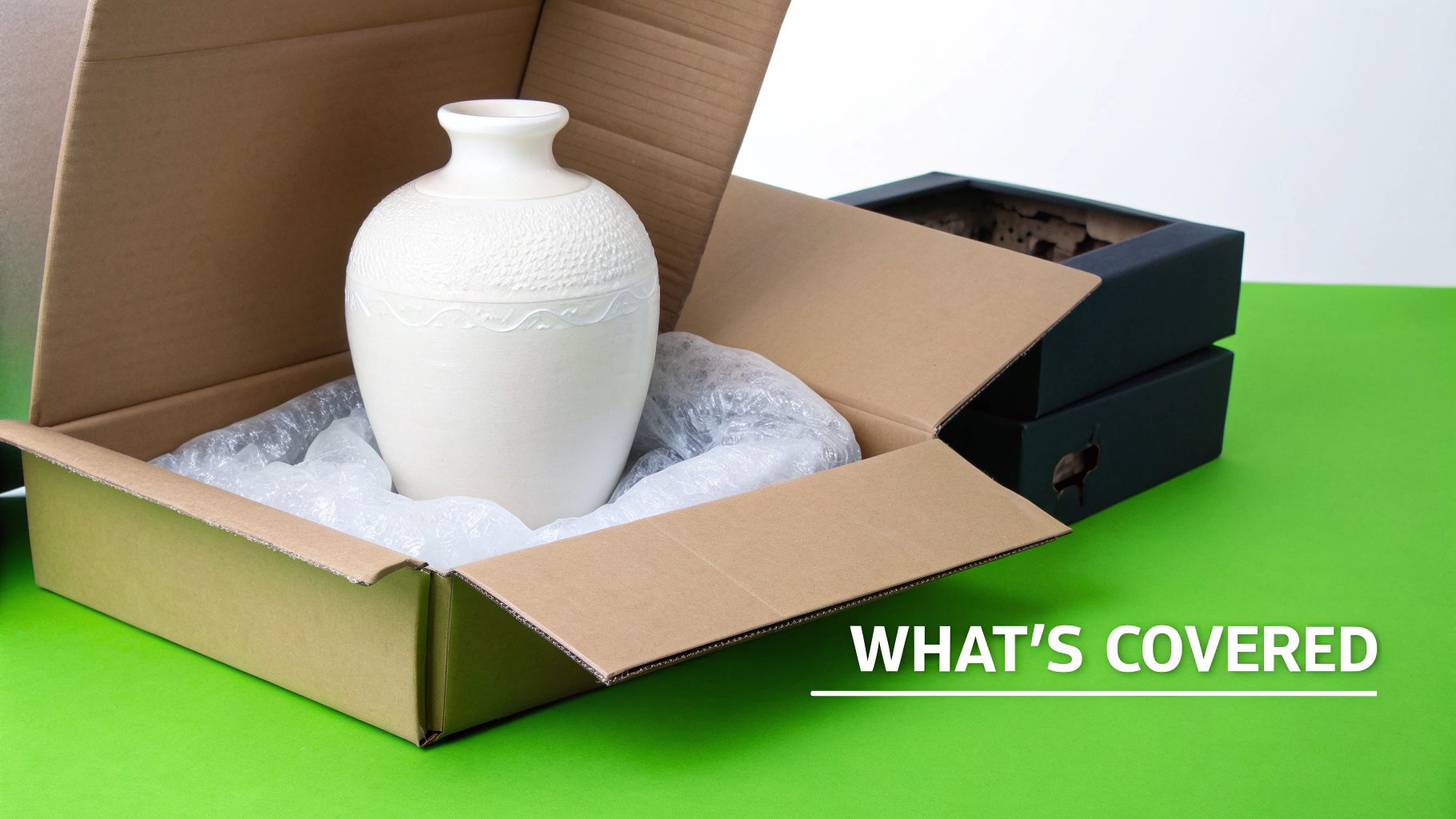

Imagine sending a beautiful ceramic vase. If you just pop it in a box with no bubble wrap or internal padding, it’s almost guaranteed to arrive in pieces. When that happens, the insurer will rightly deny the claim. Why? Because the damage was a direct result of inadequate packaging, not a courier error. The parcel simply wasn't ready for the trip.

Prohibited Items and Undeclared Goods

Every courier has a list of things they can’t or won’t carry, usually for safety, legal, or handling reasons. If you try to send prohibited goods—like flammable liquids, certain types of batteries, or perishable foods—you instantly void your insurance cover.

If a forbidden item gets lost or damaged, you won’t be able to claim for it. Period. Always take a moment to check your courier’s terms of service before you send anything, just to be sure.

Consequential Loss: What Is Not Covered

Here’s another critical exclusion you need to get your head around: consequential loss. Standard courier insurance is designed to cover one thing—the cost of replacing or repairing the physical item that was lost or damaged. That’s it.

Let’s say a marketing company sends a vital box of brochures for a major Sydney trade show. The courier loses the box. The insurance will cover the $500 it costs to reprint those brochures. What it will not cover is the $10,000 in potential sales the business missed out on by not having them at the event. That lost profit is a "consequential loss," and it falls outside the scope of a typical policy.

Understanding this helps you set realistic expectations. To get a clear picture of how we protect your goods, you can explore our guide on our included insurance and see exactly what’s covered.

Calculating the True Cost of Protecting Your Shipments

Thinking of courier insurance as just another expense is like calling a seatbelt a fashion accessory—it completely misses the point. The real value isn't in the line item on your budget; it’s in what that small cost buys you: certainty, peace of mind, and the ability to stand by the promises you make to your customers.

The true cost isn't what you pay for the premium. It's the massive, unpredictable financial hit you'd take if a shipment vanished or arrived in pieces. This is about making a smart, strategic investment in your brand's reputation and your bottom line. Every parcel you send is a handshake with your customer, and the right insurance ensures you can always follow through.

The Building Blocks of Insurance Pricing

To get a real handle on the costs, you need to look at the moving parts that make up an insurance quote. Understanding these elements puts you in the driver's seat, allowing you to balance your budget with your appetite for risk.

It all boils down to three key things:

- Premiums: This is the fee you pay for the policy itself. It's calculated based on the declared value of your goods and the perceived risk of the journey.

- Deductibles (Excess): This is the slice of the claim you agree to pay yourself before the insurance company steps in. Opting for a higher excess can often lower your premium, but make sure it’s an amount you're comfortable covering if something goes wrong.

- Coverage Limits: This is the absolute maximum the insurer will pay out for a claim. It’s vital to make sure this limit is high enough to cover the full replacement cost of your most valuable shipments.

When Standard Cover Just Won't Cut It

For everyday, low-value items, the basic liability included with a courier service like Aeros is often all you need. But the moment you're sending something with a higher price tag, the entire equation changes. Shipping a $2,000 piece of custom equipment or a bespoke designer garment with only standard cover isn't a calculated risk—it's a gamble.

Let’s put some numbers to it. A typical rate for extra cover in Australia hovers around 2.5% of the insured value. For instance, Australia Post’s ‘Extra Cover’ uses a similar rate for items valued over the standard $100 limit, with a cap of $5,000.

A Practical Example: To insure that $2,000 piece of electronics, you might pay around $50. Now, weigh that up. Is it better to invest $50 to guarantee its safety, or risk losing the entire $2,000 if the uninsured parcel gets stolen or crushed? The answer is a no-brainer.

That small, predictable cost turns a potential financial disaster into a manageable business expense. It’s a proactive move that protects your cash flow and stops one bad day from derailing your entire month. To get a clear picture of your total expenses, it helps to use tools that let you accurately calculate shipping costs.

And remember, protecting your assets goes beyond just the parcel. You can even save on premiums with anti-theft devices for cars insurance, which helps control your overall operational costs.

Ultimately, investing in extra cover isn’t about expecting the worst. It’s about planning for the best—for your business, your products, and your customers. It’s a mark of professionalism.

A Step-By-Step Guide to a Successful Claim

When a shipment goes wrong, your response in the first 24 hours can make or break your claim. It’s easy to feel a sense of panic when a customer calls about a damaged parcel, but having a clear plan transforms that chaos into a series of calm, manageable steps.

This isn’t about picking a fight; it’s about clear communication and giving your courier the right information to sort things out. Think of yourself as building a case. Every photo, every document, every detail adds another layer of strength to your position, putting you firmly in control.

Step 1: Act Immediately and Document Everything

The moment you or your customer spots a problem, the clock is officially ticking. Don't put it off. The absolute first thing to do is capture solid evidence before anything gets moved, tidied up, or thrown away.

Here’s your immediate action plan:

- Take Clear Photographs: Grab your smartphone and take plenty of well-lit photos from every angle. You need shots of the damaged item itself, the internal padding (or lack of it), and all sides of the box. Pay special attention to any punctures, crushed corners, or water stains.

- Preserve All Packaging: This is a big one. Do not throw out the box, bubble wrap, or any packaging materials. Assessors need to see exactly how the item was packed to rule out poor packaging. Tossing it in the bin is one of the quickest ways to get a claim denied.

- Jot Down the Details: Make a quick note of the date and time the damage was found, the tracking number, and a simple description of what happened.

This initial evidence is the foundation of your entire claim. Without it, you’re trying to build a house on sand.

Step 2: Notify Your Courier Promptly

Every courier has a strict window for reporting damage or loss—often as short as 24 to 48 hours from delivery. If you miss this deadline, your claim can be automatically rejected, no matter how good your evidence is.

Find your courier’s official claims channel, which is usually an online portal or a specific email address, and lodge your initial notification. Just provide the tracking number and a brief summary of the issue. This gets your claim into their system and officially registers the incident within their required timeframe.

Pro Tip: Always keep a record of your notification. Save a copy of the email or screenshot the confirmation page from the online portal. This is your proof that you acted on time.

Step 3: Gather Your Essential Paperwork

Once you’ve reported the incident, the next job is to pull together the documents that prove the item's value and the cost of the loss. Insurers can't just take your word for it; they need concrete proof.

Your documentation checklist should include:

- Proof of Value: This is usually the invoice from your supplier or the sales receipt showing what your customer paid. A screenshot of a retail website won't cut it—you need a real transactional document.

- Proof of Shipping: The consignment note or shipping label is absolutely vital. If you need a refresher, check out our guide on what is a consignment note and why it’s so important.

- Photos of Damage: Add the clear, detailed images you took back in Step 1.

- Repair Quote (If Applicable): If the item can be fixed, getting a formal quote from a reputable repairer can really speed things up. It’s almost always cheaper for the insurer to approve a repair than a full replacement.

Get these files organised into a dedicated folder on your computer. Having everything ready to go shows you’re professional, prepared, and serious about the claim.

Step 4: Submit Your Claim with Precision

Now it’s time to put it all together. Head to the courier’s claims portal or follow their submission process, filling out all the required fields with care and accuracy.

Stick to the facts in your descriptions. Avoid emotional language and simply state what the item was, its value, how it was packed, and what went wrong. When you present a claim that’s well-documented, professional, and on time, you give the claims assessor everything they need to do their job. It’s the best way to turn a shipping disaster into a resolved issue.

Taking Control: Your Guide to Minimising Shipping Risks

Let's be honest—the best insurance claim is the one you never have to make. While having a solid policy is your ultimate safety net, the real magic happens when you shift from a reactive mindset to a proactive one. It’s all about building a resilient shipping process that protects your products, your reputation, and your bottom line from the get-go.

This isn’t about adding more tasks to your already long list. It's about taking control. Every box you pack with care and every label you print with precision is a powerful step toward minimising risk and strengthening your business.

Master the Art of Defensive Packaging

Think of your packaging as more than just a box; it’s a suit of armour for your products. Its one and only job is to shield your items from the realities of transit—from rattling along conveyor belts to the inevitable bumps on the road. Getting this right is the foundation of a successful delivery and, if needed, a successful insurance claim.

Here are the non-negotiables for packing like a pro:

- Choose the Right Box: Start with a new, sturdy, double-walled cardboard box. It should be just a little larger than what you're sending. Reusing old boxes might seem thrifty, but they’ve lost most of their structural strength and just aren't worth the risk.

- Cushion, Cushion, Cushion: Aim for at least 5 cm of cushioning on all sides of your item. Fill every gap with quality material like bubble wrap or packing peanuts to suspend the item firmly in the middle. If it can move, it can break.

- Seal It Like You Mean It: Grab some strong packing tape—not everyday sticky tape—and use the 'H-tape' method. This means you tape down the centre seam and then across both edges, creating a tough, reinforced seal that won't give up.

Clear Documentation Is Your Best Friend

Great packaging is only half the battle. Your paperwork needs to be just as flawless. In Australia, this isn't just good practice; it's part of your legal duty under the Chain of Responsibility laws. These rules hold you accountable for providing clear, correct information to ensure every parcel is transported safely.

Run through this checklist every single time:

- Crystal-Clear Labels: Make sure the shipping label is stuck flat on top of the box, is easy to read, and isn’t competing with any old labels or barcodes.

- Honest Declarations: Always declare the contents and value of your shipment accurately. This is the bedrock of any potential insurance claim and helps couriers handle your goods appropriately.

- Handling Instructions: If your item is delicate, use bold, unmissable labels like "FRAGILE" or "THIS WAY UP". They aren’t a replacement for good packaging, but they give handlers crucial visual cues.

When you take these steps, you transform shipping from a game of chance into a predictable, reliable part of your operation. This is how you build a process that gives both you and your customers total peace of mind.

The sheer scale of shipping in Australia really drives home why these details matter. With the local courier and parcel market projected to hit USD 11.75 billion in 2025, the volume of goods on the move is staggering. Domestic parcels, mostly zipping between population hubs on the east coast, account for a massive 62.21% of that total. It’s a powerful reminder that robust packaging is essential for every single local delivery. You can dive deeper into Australia's bustling courier market on Mordor Intelligence.

Answering Your Top Questions About Courier Insurance

Jumping into the world of courier insurance can feel a bit daunting, and it's natural to have questions. Getting the right answers is the key to making smart decisions that truly protect your business and give you peace of mind. Let's clear up some of the most common queries we hear about courier insurance in Australia.

Think of this as putting the final, crucial pieces of your shipping puzzle into place. By the end, you'll have a rock-solid understanding of your responsibilities and options, leaving no room for guesswork.

Is Courier Insurance a Legal Must-Have in Australia?

This is a great question, and the answer isn't a simple yes or no. While there’s no specific law saying you must purchase extra insurance, Australia's 'Chain of Responsibility' legislation is the real game-changer here. It means you and your courier are jointly responsible for ensuring goods are transported safely.

So, while it's not legally mandated in the traditional sense, insurance becomes a commercial necessity. It’s how you manage your financial risk and properly meet your obligations within that shared duty of care. For any serious business, it's a non-negotiable part of the process.

What’s the Difference Between Freight Insurance and Public Liability Insurance?

It's easy to get these two mixed up, but they cover completely different things. Knowing the difference is crucial for making sure your business is properly protected from every angle.

- Freight Insurance: This is all about your goods. It’s the policy that covers loss or damage to your products while they're on their journey with the courier.

- Public Liability Insurance: This protects the courier's business. It covers them if their actions cause injury to a person or damage to third-party property—like if a trolley accidentally scrapes your shop's front door during a pickup.

Key Takeaway: Freight insurance protects what's inside the box. Public liability protects the courier from accidents happening outside the box. You need the first one to safeguard your shipments.

My Fragile Item Broke in Transit. Am I Covered?

Coverage for fragile items almost always hinges on one critical detail: how well you packed it. Insurers are meticulous about this, and a claim will likely be denied if the packaging wasn't up to scratch.

To give your claim the best chance of success, you need to show you did everything reasonably possible to protect it. That means using a brand-new, sturdy box, surrounding the item with generous amounts of cushioning like bubble wrap, and plastering 'Fragile' labels all over it. The onus is firmly on you, the sender, to pack your goods to withstand the normal rigours of transit.

Ready to ship with the confidence that comes from reliable service and included protection? Aeros Couriers makes sending parcels across Australia simple, affordable, and secure. Get an instant quote and see how easy it is to protect your shipments and delight your customers.